Illustration of two men listening to a financial expert advice. Source: TechGaged

How Accurate Are Financial Experts?

In Brief

- • Financial experts often perform near chance, with accuracy akin to a coin flip.

- • Confidence and media incentives outweigh consistent predictive success.

- • Data-driven and AI approaches increasingly outperform human judgment.

In the 1996 classic Jerry Maguire, Tom Cruise famously screams, “Show me the money!” It’s a line that defined a generation’s attitude toward success. But two decades later, the everyday investor has a different demand: showing accuracy.

These days, financial forecasting is a discipline that gets people heard. For some, it also gets them a slot on a major network. For others, there are droves of followers on social media hanging on their every word. Whatever their status, they all have the power to move millions with a single sentence.

The data shows that financial expertise, in all its glory, is often less about predicting the future and more about narrating the present with extreme confidence. So, following our deep dives into some of the most influential voices out there, it’s time to question (however uncomfortable it may be) why we are still listening.

Latest Stories

US Government Seizes Crypto from Binance User Account

Digital Asset Firms Eyed by Dune Acquisition III for SPAC Merger

Bullish: Go-Ethereum Client Update Lays Groundwork for Amsterdam Hardfork

Looking for deeper insights into the future of crypto? Explore our Crypto Predictions 2026 guide covering Bitcoin forecasts, expert outlooks, and key market trends.

What the Data Says

To understand why expert advice leads to a lighter wallet more often than not, we have to focus on the numbers. The fact is, the academic world has been quietly sounding the alarm for years. Still, peer-reviewed papers aren’t nearly as exciting as a guy shouting or pushing novelty buttons with different sounds.

Let’s start with one of the more exhaustive studies from the CXO Advisory Group. They spent years grading over 6,500 specific market forecasts from 68 high-profile “gurus.” The results showed that the average accuracy rate across the board was 47%.

So, literally, it’s a coin toss whether your investment decision would backfire or not. The study highlighted that financial experts who were wrong in the past didn’t learn from their mistakes – they simply doubled down on the same biases that made them wrong to begin with.

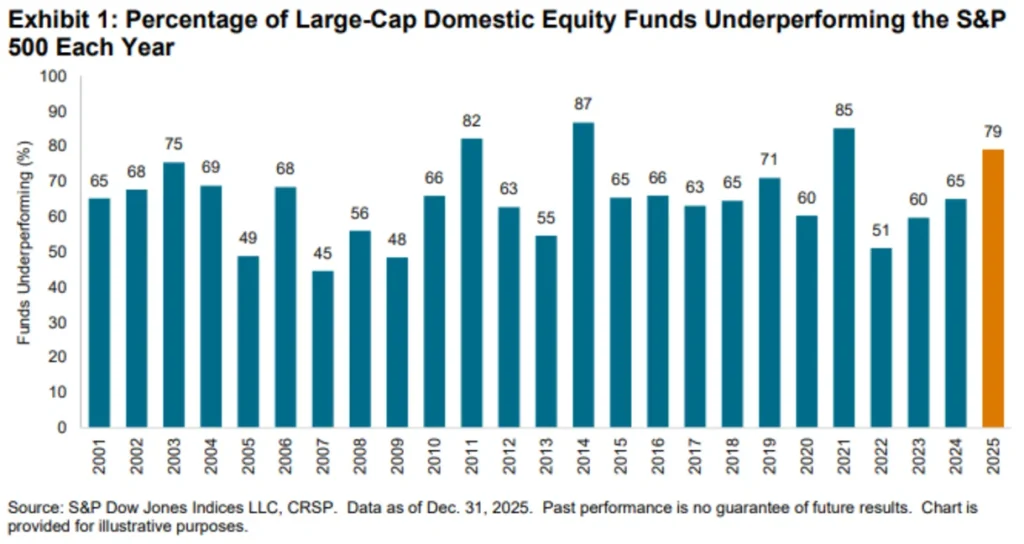

Perhaps professional fund managers are the safer bet? Perhaps not, as the SPIVA (S&P Indices Versus Active) 2025 Year-End report found that 79% of active large-cap managers underperformed the S&P 500. When you stretch that out to a 10-year horizon, the failure rate jumps to 84%.

Mind you, these are people with PhDs from the best schools money can buy. They certainly have more than enough computing power at their disposal to simulate whatever they want, yet they consistently lose in their predictions. If anything, the data suggests that know-how in finance is often a polite method of expensive guessing.

Speaking of educated people, a couple of professors of finance did an extensive study on financial professionals and their investment decisions. The duo found no evidence that financial experts are better than individual investors in that regard. They also don’t outperform or diversify their risks better, all the while having the same or higher behavioral biases.

It’s important to note that managers fare much better in stocks for which they have an information advantage over other investors, like stocks held by their mutual funds. Plus, the more experienced they are, the more aware of their investment skills they seem to be. Still, the results clearly suggest that there are limits to the value added by financial expertise.

| Expert category | Statistical reality | Primary failure reason |

| Market gurus | ~47% accuracy | Repeating the same narrative regardless of market shifts |

| Active fund managers | 79% underperformed the S&P 500 in 2025 | High management costs combined with subjective indexing |

| Institutional analysts | ~32% hit rate for 12-month price targets | Incentivized to keep ratings high for corporate client relations |

| AI | 34.7% reduction in error vs. human analysts | Can miss qualitative black swan geopolitical events |

| Long-term professionals (10 years) | 84.3% underperformed the index over a 10-year horizon | Failing to adapt to secular technological shifts (like the AI era) |

Case Studies: Jim Cramer and Robert Kiyosaki

How about we take a look at two of the most attention-commanding financial experts out there?

Jim Cramer

Our examination of Jim Cramer’s predictions revealed that the famed TV host is right about every third time or so. There were occasional big-picture wins, but his record is marred by weak consistency and poor timing.

📊 Jim Cramer Prediction Accuracy (2000–2026)

-

✓

Correct predictions: 3 / 8 (37.5%) -

✕

Short-term forecasting reliability: Low -

✓

Long-term trend spotting: Sometimes strong -

✕

Timing accuracy: Unreliable

Overall accuracy: Low (~37.5%) — occasional big-picture wins, but weak consistency and poor timing

Based strictly on 8 confirmed predictions from TechGaged dataset (2000–2026).

Equally important, our report uncovered Cramer’s psychological quirk that is amusing, at the very least. Between 2000 and 2026, Cramer isn’t necessarily a bad analyst in the sense that he lacks knowledge. It’s more like he’s a top-notch narrator and a momentum chaser.

Cramer’s biggest misses, like telling people Bear Stearns was “fine” in 2008 or calling Bitcoin a winner right before a $130 billion market cap decline, occur because he reflects the current mood of the market.

Looking back at a quarter-century of data, his buy recommendations often act as a peak sentiment indicator. By the time a stock is discussed on national television with that much enthusiasm, the smart money has already moved on, leaving the retail investor to hold the bag.

That’s why the Inverse Cramer is a thing to begin with. After all, Cramer is a TV personality, first and foremost. Hence, his primary job is to keep you engaged, not necessarily to make (and keep) you rich.

Robert Kiyosaki

On the other end of the expert spectrum, we have the doomsday prophet. As we noted in our investigation into Robert Kiyosaki’s predictions, his brand is built on a broken clock philosophy. He has strong macro insight, but rather weak timing precision.

📊 Kiyosaki Prediction Accuracy (1990–2026)

-

✓

Correct predictions: 3 / 7 (~43%) -

✕

Short-term forecasting reliability: Low -

✓

Macro direction: Often correct -

✕

Timing accuracy: Unreliable

Overall accuracy: Low to Moderate (~43%) — strong macro insight, weak timing precision

Based strictly on 7 confirmed predictions from TechGaged dataset (1990–2026). One prediction remains ongoing.

It works like this: if you predict a giant crash every Tuesday for years – nay, decades, at this point – you will eventually be right. However, the wealth lost while waiting for the economy and the financial world to end is close to astronomical.

Since 2011, an investor who stayed in a broad-market index fund would have outperformed Kiyosaki’s recommended “hard assets” (gold and silver) by nearly 400%.

Granted, Kiyosaki correctly identifies structural issues, such as the staggering rise in national debt. The problem is that his solution is almost always to exit the system. To make matters worse, his timing is designed to trigger survival instincts, as opposed to maximizing ROI.

In the 2020s, that advice has been a major misstep for those who missed the most concentrated wealth-creation event in history, which was the digital and AI revolution. Fear is a potent sales tool, but it’s a poor investment strategy, as reflected by Inverse Kiyosaki and other examples.

Want to explore the bigger picture behind the numbers? Explore our full cryptocurrency statistics report for deeper insights into market growth, adoption, and blockchain trends.

Are We Internally Wired to Follow Financial Experts?

It seems that we are, and it’s no small part as to why financial experts get book deals and whatnot.

The human brain is designed to remember intense emotional experiences (like fear or shock) over mundane ones. It helps our survival, which means we are biologically wired to remember hits and forget misses.

A predicted crash is perceived as a form of threat or high-drama event, making it more emotionally engaging and thus, more memorable, than routine stuff.

Then, there’s the cognitive bias. As a species, we often trust the feeling of certainty more than the evidence itself. Confident speakers, regardless of their actual performance, are perceived as more knowledgeable because our brains treat confidence as a mental shortcut for expertise.

In other words, if someone screams with enough conviction, our brains tend to bypass the part that asks for proof.

Lest we forget, the media incentive plays a huge role here. Controversy and extreme predictions drive clicks. A nuanced analyst saying that the market will likely grow 7% over the next decade with some volatility doesn’t get views and likes. But a guy saying that the dollar is dying and you need to buy zinc or whatever gets a headline.

In the end, it would be easy to attribute this tendency of ours to a personal failing. It’s not. It’s an evolutionary trait designed to create quick narratives from incomplete information, often at the expense of accuracy.

How Good Are AI Models?

Now, this may be worth your effort and, possibly, money, as several studies point out that AI is onto something here.

For instance, one recent study pitted a group of seasoned sell-side analysts against a specialized neural network to predict 12-month price targets. The AI model achieved a 34.7% reduction in forecasting error compared to its human counterparts.

What’s more, the data unveiled that human analysts were 8.7% more likely to issue reports heavily based on optimism. Basically, they were inflating targets to maintain corporate relationships or please big clients.

Because AI-integrated financial models have no social anxiety or corporate incentives, they remained focused strictly on the data at hand, leading to far more realistic (and profitable) risk assessments.

When it comes to technical reasoning, the gap is even wider.

Designed specifically for contextual reasoning in regulated financial domains, an advisor-grade AI system scored an average of 98.3% on complex financial reasoning tasks, such as tax-loss harvesting and multi-account optimization. In contrast, the human Certified Financial Planners had an average of 79.5%.

Also, with humans, the accuracy dropped by nearly 15% during high-volatility market events due to emotional stress and information overload. On the other hand, the AI models maintained a stable performance of 95 to 97%.

The fact is that modern machine learning models operate with a cold, mathematical precision that is increasingly difficult to match. Yet, some data show that a hybrid system, which uses machine learning for the quantitative heavy lifting but includes a human for ethical and contextual oversight, may be the best solution.

In this model, the AI would provide a counterpoint when humans systematically overestimate growth to please corporate clients. They’d offer more pessimistic, but accurate risk indicators while the human makes strategic judgments in terms of understanding customer goals, weighing pros and cons, anticipating regulatory responses, and shedding light on long-term consequences.

A New Dawn of the Expert Era?

Is it safe to assume that in the next few years, financial expertise will be defined by AI models? The data certainly steers toward that conclusion.

AI-driven financial frameworks are en route to becoming more accessible to the average investor. As a result, there will be less reliance on good old-fashioned financial gurus as personalized quantitative analysis slowly pushes them out.

Instead of factoring in what someone thinks about the dollar, investors will be using localized models to run simulations on their specific portfolios in real time.

So, how can a human compete with a machine that accounts for raw sentiment data, institutional flow, real-time supply chain metrics, and everything else?

By being flashy and bombastic – things that AI will likely never be.

The central paradox of financial expertise is that the more “out there” an expert becomes, the more their accuracy tends to degrade. They’ve bred a cult that, unfortunately, forces them to take binary stances. Yet, the systems they take these stances on are inherently chaotic and non-linear.

That’s why high-profile financial experts like Cramer and Kiyosaki provide a new pick virtually every day: they cater to the broadest denominator. They must do so to keep their audiences engaged and their brands prophetic. And despite their low accuracy, they can do so freely because the penalty for being wrong is zero.

In a weird way, that is their very incentive.

So, as an investor, you should look past the charismatic delivery and prioritize transparency and math over charisma. Listen to the quiet signals of your long-term goals and risk tolerance, as these are the metrics that no expert can ever know. And if you must listen to one, use them to see which way the wind of public sentiment is blowing.

In the financial world of high-speed change, the boring path is usually the one that leads to money.

Methodology: This report cross-references various academic studies, along with independent performance tracking of Jim Cramer and Robert Kiyosaki. We focused on the gap between predicted outcomes and actual market performance over a 20-year window.

Disclaimer: The information provided in this article is for educational and informational purposes only and is based on documented public facts. This is not financial advice. Techgaged does not provide investment recommendations, and the historical performance of any individual mentioned in this piece is not a guarantee of future market results.

FAQs

How accurate are financial experts at predicting markets?

Most data suggests that financial experts perform no better than chance. For example, a large-scale study by CXO Advisory Group found an average accuracy rate of just 47%, essentially equivalent to a coin flip. Even professional fund managers frequently underperform benchmarks like the S&P 500 over the long term.

Why do people continue to trust financial experts despite poor track records?

Human psychology plays a major role. We’re wired to remember bold, emotional predictions (like market crashes) more than routine outcomes, and we often equate confidence with competence. Media incentives also amplify extreme opinions, making charismatic experts more visible and influential than consistently accurate ones.

Are individual investors really worse than professionals?

Surprisingly, not necessarily. Research shows that financial experts often don’t outperform individual investors in returns or risk management. In some cases, they exhibit the same or even stronger behavioral biases, despite having more education and resources.

How do well-known experts like Jim Cramer and Robert Kiyosaki perform?

Both illustrate different weaknesses in financial forecasting. Jim Cramer tends to reflect market sentiment, often making calls that align with peaks in hype. Robert Kiyosaki, on the other hand, frequently predicts major economic collapses but struggles with timing, leading to missed long-term gains for followers.

Can AI outperform human financial experts?

Increasingly, yes. Studies show that AI models can significantly reduce forecasting errors and maintain consistent performance even during volatile markets. Unlike humans, they aren’t influenced by emotions or external incentives, making their predictions more data-driven and stable.

What’s the best way to use expert opinions as an investor?

Rather than treating experts as guides, it’s often more effective to view them as indicators of market sentiment. Prioritizing long-term strategy, personal risk tolerance, and data-driven decision-making tends to yield better results than following bold predictions or media personalities.

How do you rate this article?

Subscribe to our YouTube channel for crypto market insights and educational videos.

Join our Socials

Briefly, clearly and without noise – get the most important crypto news and market insights first.

8

Also read

Similar stories you might like.

Crypto News

Ripple CEO Criticizes Strategy’s Bitcoin Model, Stays Bullish On BTC

TechGaged | 2026-06-30

Crypto News

BlackRock Has Sold ETH for 7 Straight Days — Is Institutional Sentiment Changing?

Azeez | 2026-06-30

Crypto News

84% of Altcoins in ‘Total Underperformance’, Bitcoin Moving to $58K

Ana | 2026-06-30

Crypto News

CZ Questions Reports of His Rising Riches Despite Market Drop, Gets Hit With Backlash

Ana | 2026-06-29

Crypto News

Bitcoin Fails to Hold $60K, ETFs Continue Pressuring Market

Ana | 2026-06-29

Crypto News

Wall Street-Style Capital Enters DeFi: Bitwise Stakes Millions in HYPE

Azeez | 2026-06-28

Crypto News

Down $1.7B, SharpLink Resumes Buying Ethereum

TechGaged | 2026-06-26

Crypto News

Bitcoin Dips Below $59K as ETFs Let Go of $696 Million and Options Expire

Ana | 2026-06-26

Crypto News

BitGo Cuts Jobs to Prioritize AI and Stablecoins

Ana | 2026-06-26

Crypto News

The Market Event Every Crypto Trader Is Watching

Azeez | 2026-06-26