Bitcoin coins. Source: TechGaged / Shutterstock

4 Events That Could Break Michael Saylor’s Bitcoin Strategy

In Brief

- • Strategy relies on its stock trading above its Bitcoin value.

- • Weak Bitcoin prices during debt maturities raise repayment risks.

- • Regulatory changes could disrupt key funding channels.

Ad

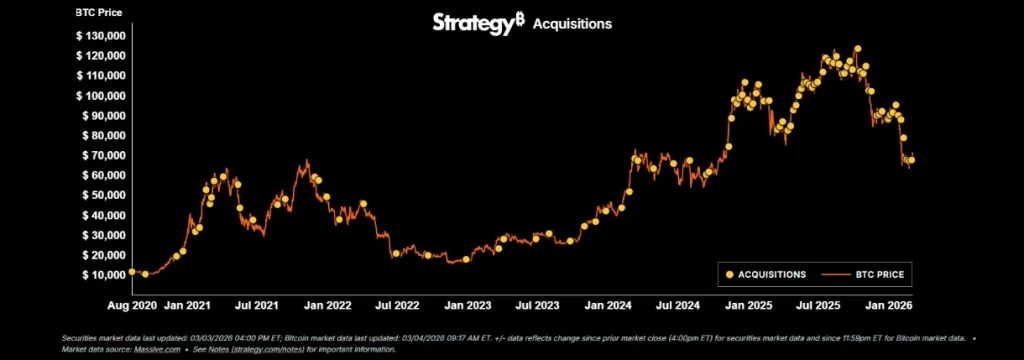

It’s no secret that Michael Saylor has turned Strategy into a Bitcoin-buying machine due to its unconventional strategy. That machine keeps relentlessly rolling, as on March 2nd, 2026, the company announced the purchase of 3,015 BTC, adding to its total of 720,737.

While that makes for great headlines, the how is just as interesting as the why.

To offset falling prices and keep the crypto dream alive during market dips, Saylor has essentially flooded the market with new shares at a record-breaking pace. In fact, he’s been doing so unlike almost any other major US firm.

It’s a move (and arguably a point of pride at this point) that keeps Strategy’s Bitcoin hoard growing, but for the average shareholder, it comes with a side of heavy dilution and significant risk.

As such, there is no shortage of skepticism regarding the viability of Saylor’s business model. Upon closer look, the worries are far from unfounded.

How Strategy finances its Bitcoin purchases

From a historical perspective, the company’s most frequent tool for funding its Bitcoin treasury is the At-the-Market (ATM) offering. As opposed to a traditional stock sale where a company dumps a massive block of shares at a discount, an ATM offering acts in a more controlled manner. Strategy instructs brokers to sell shares incrementally into the open market at the current market price.

Doing so minimizes the sudden price drops usually caused by large share issuances. Therefore, the ATM strategy is most effective when the stock trades at a premium to its market net asset value (mNAV), which is a metric comparing the company’s market cap to the market value of its Bitcoin holdings.

When the stock is considered expensive compared to the Bitcoin it holds, Strategy sells a small amount of equity to buy a disproportionately large amount of Bitcoin, making the move accretive (beneficial) for existing shareholders.

At the heart of this operation is a proprietary metric Saylor calls Bitcoin yield. Simply put, it tracks the percentage change in the ratio between the company’s total Bitcoin holdings and its share count. The idea isn’t just to own more Bitcoin but to see to it that the amount of Bitcoin backed by each share is constantly increasing, even as new shares are printed.

In cases where the equity market is less favorable or when Saylor and co. want to move faster, they shift to convertible debt and preferred stock, often referred to by the ticker STRC or Stretch.

Strategy is fairly famous for issuing billions in zero-coupon bonds. These are basically interest-free loans from institutional investors. In exchange for zero percent interest, lenders get a call option, which is the right to convert that debt into Strategy stock if the price hits a certain target.

In other words, it’s a bet on the future where Saylor gets cash to buy Bitcoin today, while lenders get a low-risk way to bet on the stock’s upside.

Where the (potential) problem is

There is no denying that the Bitcoin yield math looks good on a spreadsheet, but the real world has a nasty habit of throwing wrenches into even the most elegant financial machines. For Strategy, the risks aren’t just about the price of Bitcoin but rather about the fragile relationship between three elements: stock price, the company’s debt, and its ability to keep the flow going.

When the premium flips

The entire model of using ATM offerings to buy Bitcoin relies on a stock premium, where investors are willing to pay more for the Strategy stock than the Bitcoin it holds is actually worth. When this premium is high, Saylor can print shares to buy “cheap” Bitcoin for his holders.

However, Bloomberg data from early 2026 shows things may be grinding to a halt.

Over the past 12 months, Strategy’s stock has plummeted nearly 50%, far outstripping the decline in Bitcoin itself. As the premium compresses, the ATM drip effectively dries down. If the stock trades at or below its mNAV, selling new shares becomes dilutive, meaning it reduces the amount of Bitcoin each existing share represents. In turn, doing so would punish current investors.

This premium exists largely because Strategy acts as a regulated gateway. Many massive institutional funds are legally barred from buying Bitcoin directly on an exchange, though they are allowed to buy shares in a US software company. This proxy status creates an artificial demand that keeps the stock price higher than the value of its coins, at least until the market’s appetite disappears.

Without the premium (if the market loses faith in it), the company’s main growth engine doesn’t just slow down – it simply stops.

$8,000 stress test against business reality

In a flurry of February 2026 interviews, Saylor attempted to calm nerves after Strategy CEO Phong Le mentioned in December 2025 that there was a scenario in which the company could sell some Bitcoin, based on how far Strategy’s market capitalization and Bitcoin prices fall. Saylor cited a specific figure: $8,000.

He argued that even if Bitcoin crashed by 90%, the company would not be forced to sell. In an interview with CNBC, his specific words were:

“If Bitcoin falls to $8,000, we’ll just refinance the debt. We’ve got 2.5 years of cash on the balance sheet just to cover interest and dividends. We aren’t sellers; we’re buyers forever.”

But, there is a point to be made that the $8,000 figure is a liquidation price, not one that a business model hinges on.

While the company might technically survive at $8,000, its ability to function as a growth vehicle would be nonexistent. With an average Bitcoin purchase price now sitting near $76,000, a drop to $8,000 would result in an unrealized loss of nearly $48 billion.

Survival is one thing, but being a viable investment for shareholders while sitting on a 90% loss is another thing entirely.

Debt maturity wall

Perhaps the most fascinating aspect of Saylor’s maneuvering is his 0% interest deals. At first, these are brilliant, but the issue is what happens when they expire.

These convertible notes have expiration dates between 2027 and 2032, with the goal to swap the debt for shares so the company never has to pay back the cash. The risk here is that in case the stock stays in the valley of despair (a term Saylor recently used to highlight Bitcoin’s struggles and likening it to Apple’s 2012), lenders won’t want the stock. They’ll want their cash.

Hence, the problem is a stagnant market rather than a sudden crash. Considering that Strategy is reporting massive unrealized losses that some estimates put at $9.5 billion, the company doesn’t have the spare cash to pay those billions back without selling its Bitcoin stash.

Still, selling Bitcoin to pay debt is the ultimate reverse scenario, and one that could force Saylor’s hand long before Bitcoin ever hits $8,000.

Developments that would lead to the bust scenario

For Michael Saylor’s strategy to collapse, the company would likely need to hit a perfect storm of these four major developments:

- Strategy stock begins trading at a persistent discount to its mNAV. Once the stock price is lower than the value of the Bitcoin it holds, the ATM route is useless. Selling shares would actively destroy value for existing holders, leading to dilution without gain. If investors stop believing that Strategy’s stock is higher than the dollar value of the Bitcoin in its vault, the company loses its ability to buy more Bitcoin without taking on massive, expensive debt.

- Bitcoin stays flat (e.g., stuck between $40k and $60k) for several years, coinciding with the 2027–2030 debt maturities. Strategy relies on the stock price being high enough that lenders really do want to convert their debt into shares. But if the stock is underwater when the bills come due, lenders will most certainly demand cash, not stock. And since the cash is all tied up in Bitcoin, Strategy would be forced to sell its BTC into a stagnant market to pay back billions in principal. Ironically, this would be the exact type of forced selling that Saylor promises will never happen.

- New regulations or a banking crisis make it illegal or prohibitively expensive for institutional yield-seekers to buy Strategy’s convertible notes. This links to Saylor’s 0% interest loans that depend on hedge funds being able to monetize the stock’s volatility. If the SEC or banking regulators tighten the screws on corporate debt linked to digital assets, perhaps by requiring higher capital reserves or stricter disclosure on Bitcoin-related securities, that source of interest-free cash dries up.

Several smaller red flags would signal the end is near, such as a negative Bitcoin yield. If Strategy reports a quarter where the amount of Bitcoin-per-share decreases, it proves the math has flipped against it.

Then, there is the margin call at $8,000. While Saylor is adamant that Strategy can refinance, a drop to this level would likely trigger cross-default clauses in smaller loans or preferred stock agreements. At this price, the collateral value of the Bitcoin stash would be so low that it’s hard to see how any bank would offer a new loan to roll over the old ones.

It’s not far-fetched to see a potential legal injunction down the road. Strategy’s transition from a software company to a de facto Bitcoin treasury company has attracted intense scrutiny, resulting in a class-action lawsuit alleging that executives made misleading statements about the profitability and risks of their Bitcoin strategy. If Strategy were barred from issuing new securities, that would stop it in its Bitcoin-buying tracks.

We also can’t forget the original business that Strategy is in. While the world focuses on the Bitcoin treasury, the company’s legacy enterprise software business remains the vital cash cow that generates the actual revenue needed to pay interest on its non-zero debt. In the event the software side of the house falters, Strategy loses the foundational cash flow that supports its aggressive borrowing, likely turning a bold treasury strategy into a desperate survival play.

Conclusion

One thing is certain: Michael Saylor doesn’t do things by halves. Perhaps that’s why Strategy dropped ‘Micro’ from its name.

But in all seriousness, the company has evolved into a high-stakes experiment in corporate leverage. The model is a masterpiece of financial engineering when Bitcoin is trending up and the so-called Saylor premium is intact, allowing the company to stack assets at a pace no other firm can match.

Nonetheless, as explored in this article, Strategy’s machine relies on a delicate balance of market conditions, regulatory leniency, and investor faith.

If Bitcoin enters a multi-year valley of despair or if the regulatory environment shifts, the very tools used to build this treasury (ATM offerings and 0% debt) could quickly become the weights that pull it down.

For now, Saylor and the rest of the team are betting everything that the math of Bitcoin yield will outrun the reality of Strategy’s debt maturities. Whether Saylor is a visionary pioneer or the architect of a historic corporate bust will likely depend on where Bitcoin sits when the bills finally come due in 2027.

How do you rate this article?

Subscribe to our YouTube channel for crypto market insights and educational videos.

Join our Socials

Briefly, clearly and without noise – get the most important crypto news and market insights first.

8

Also read

Similar stories you might like.

Industry

Pakistan Launches National Crypto Regulator; What’s Next?

Rokas | 2026-03-06

Altcoins

DOGE Forms Bullish Falling Wedge Against Bitcoin; What It Means

Rokas | 2026-03-06

Bitcoin

Bitcoin Wallets Hit Record 58.45M As Exchange Supply Falls

Ana | 2026-03-06

Bitcoin

Large Jane Street Bitcoin Transfers Detected Onchain

Ana | 2026-03-06

Industry

Russia Proposes Crypto Exchange Licenses For Banks

Ana | 2026-03-06

Altcoins

XRP Rally Could Exceed 600%, Analyst Says

Rokas | 2026-03-05

Bitcoin

Bitcoin Overlay With Nikkei Points To Multi-Year Rally

Ana | 2026-03-05

Altcoins

Ethereum Trader Turns One Trade Into Nearly $1M; Here’s How

Ana | 2026-03-05

Altcoins

XRP ETFs Cross $1B Assets As Investors Accumulate; What’s Next?

Ana | 2026-03-05

Bitcoin

Bitcoin Hashrate Surges 50% In One-Month Recovery – What It Means

Rokas | 2026-03-05